Table of Contents

Definition

A Trial Balance is a list of balances on the accounts in the ledger at a certain date. (Coucom, C. (n.d.). IGCSE & O-Level Accounting.)

Objectives & Advantages of Trial Balance

- It checks the arithmetical accuracy of ledger accounts

- It gives material for preparing final accounts

- To have a proof that the double entry of each transaction is made

Important Keys Points When Preparing A Trial Balance

- It should be remembered that all the assets, drawings, and expenses accounts are always debited

- All liabilities, capital and incomes are always credited

- Closing stock is never recorded in a trial balance

- Opening stock (stock at the beginning of the accounting period) is treated as asset and hence debited

- Debit total and credit total are equal

- If debit total and credit total are not equal then the difference is transferred to suspense account/labelled as “suspense a/c difference” in the trial balance

Simplified Table of Accounts Belonging to Debit or Credit Side

| Debit Side/Debit Balances | Credit Side/Credit Balances |

| Assets | Liabilities |

| Expenses | Incomes |

| Drawings | Capital |

| Purchases | Sales |

| Sales Returns | Purchases Returns |

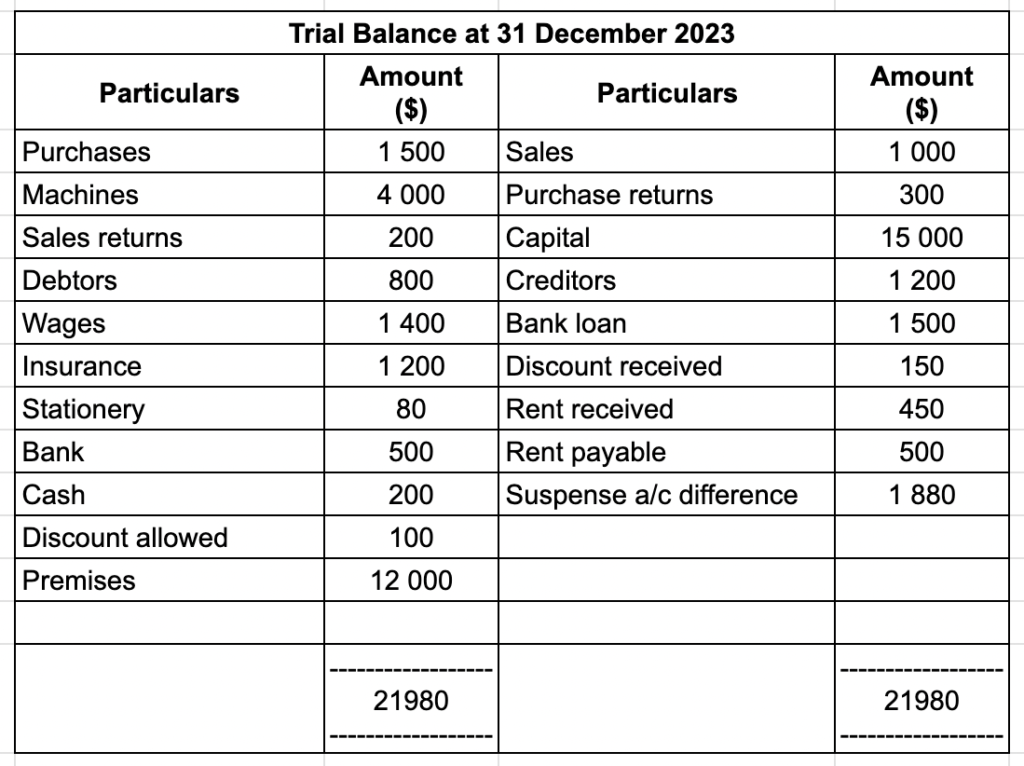

Example Question 1

Test your knowledge with the following question!

First identify what elements of accounting to these accounts belong to, whether it is asset or income, then identify whether it has a debit or credit balance (i.e. which side it should be written in the trial balance):

| Sales a/c | Income | 1 000 | Cr | Stationary a/c | Expense | 80 | Dr |

| Purchases a/c | 1 500 | Bank a/c | 500 | ||||

| Machines a/c | 4 000 | Cash a/c | 200 | ||||

| Sales returns a/c | 200 | Bank loan a/c | 1 500 | ||||

| Purchases returns a/c | 300 | Discount allowed a/c | 100 | ||||

| Capital a/c | 15 000 | Discount received a/c | 150 | ||||

| Creditors a/c | 1 400 | Rent received a/c | 450 | ||||

| Debtors a/c | 800 | Premises a/c | 12 000 | ||||

| Wages a/c | 1 400 | Rent payable a/c | 500 | ||||

| Insurance a/c | 1 200 |

Answer

Let us fill in the table to identify which element each account belongs to and what type of balances do they have:

| Sales a/c | Income | 1 000 | Cr | Stationary a/c | Expense | 80 | Dr |

| Purchases a/c | Expense | 1 500 | Dr | Bank a/c | Asset | 500 | Dr |

| Machines a/c | Asset | 4 000 | Dr | Cash a/c | Asset | 200 | Dr |

| Sales returns a/c | Expense | 200 | Dr | Bank loan a/c | Liability | 1 500 | Cr |

| Purchases returns a/c | Income | 300 | Cr | Discount allowed a/c | Expense | 100 | Dr |

| Capital a/c | Capital | 15 000 | Cr | Discount received a/c | Income | 150 | Cr |

| Creditors a/c | Liability | 1 400 | Cr | Rent received a/c | Income | 450 | Cr |

| Debtors a/c | Asset | 800 | Dr | Premises a/c | Asset | 12 000 | Dr |

| Wages a/c | Expense | 1 400 | Dr | Rent payable a/c | Liability | 500 | Cr |

| Insurance a/c | Asset | 1 200 | Dr |

Now, let us put them in a Trial Balance: (super duper easy)

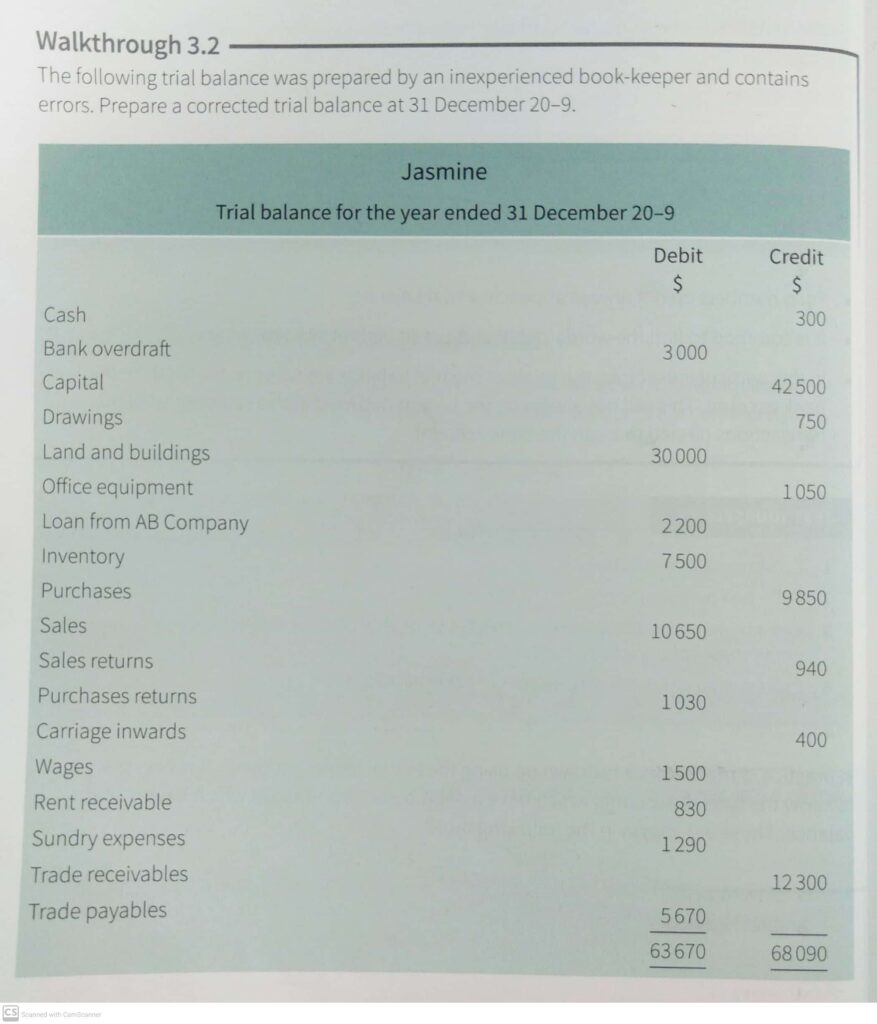

Example Question 2

There are errors in the following Trial Balance. Can you identify them?

To avoid confusion, let us first identify the elements of each of those accounts!

| Particulars | Element | Amount | Dr/Cr |

| Cash | Asset | 300 | Dr |

| Bank overdraft | Liability | 3 000 | Cr |

| Capital | Capital | 42 500 | Cr |

| Drawings | Drawings | 750 | Dr |

| Land and buildings | Asset | 30 000 | Dr |

| Office equipment | Asset | 1 050 | Dr |

| Loan from AB Company | Liability | 2 200 | Cr |

| Inventory | Asset | 7 500 | Dr |

| Purchases | Asset (long term)/Expense (short term) | 9 850 | Dr |

| Sales | Income | 10 650 | Cr |

| Sales returns | Expense (faulty goods returned by your buyer) | 940 | Dr |

| Purchases returns | Income (review Topic 2 Part A if you’re confused) | 1 030 | Cr |

| Carriage inwards | Expenses | 400 | Dr |

| Wages | Expenses | 1 500 | Dr |

| Rent receivable | Income | 830 | Cr |

| Sundry expenses | Expenses | 1 290 | Dr |

| Trade receivables (aka. debtors) | Assets | 12 300 | Dr |

| Trade payables (aka. creditors) | Liability | 5 670 | Cr |

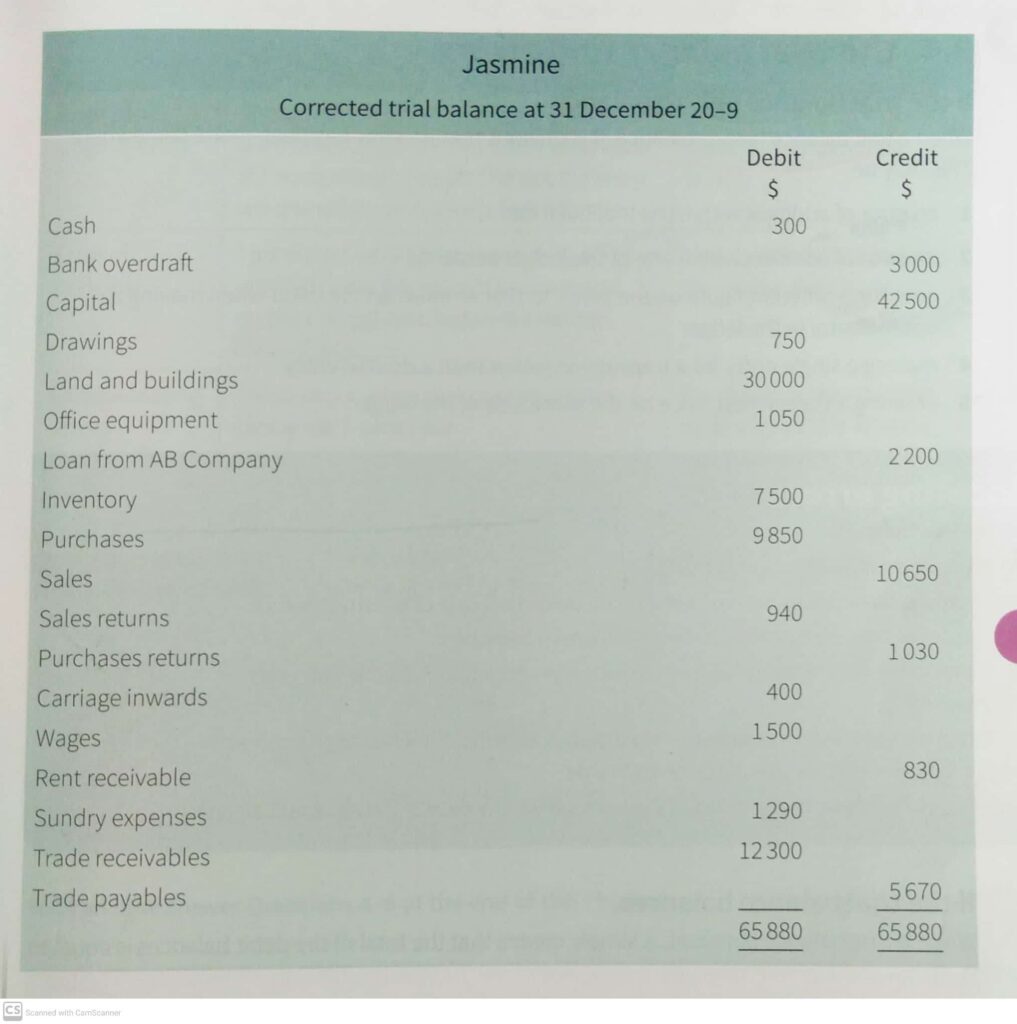

Answer

Now, we put them in a Trial Balance:

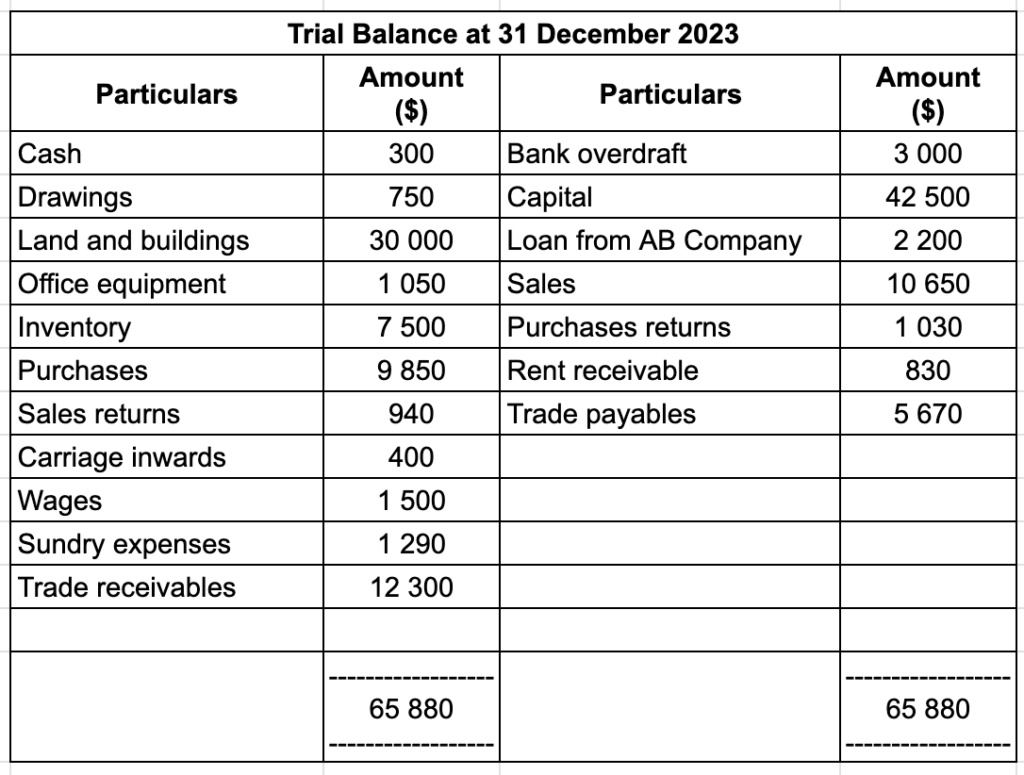

Another format would look like this:

Feel free to use any of the 2 formats when making a Trial Balance. Just ensure that the ending should be “Trial Balance at…”. I used the one my teacher taught me (cause I felt like it was simpler), and it got accepted during IGCSE exams.

Use the one you think is easier to draw. If you feel like, “hmm, the one in the textbook I think is easier..” then go ahead and use it! ^^

Example Question 3

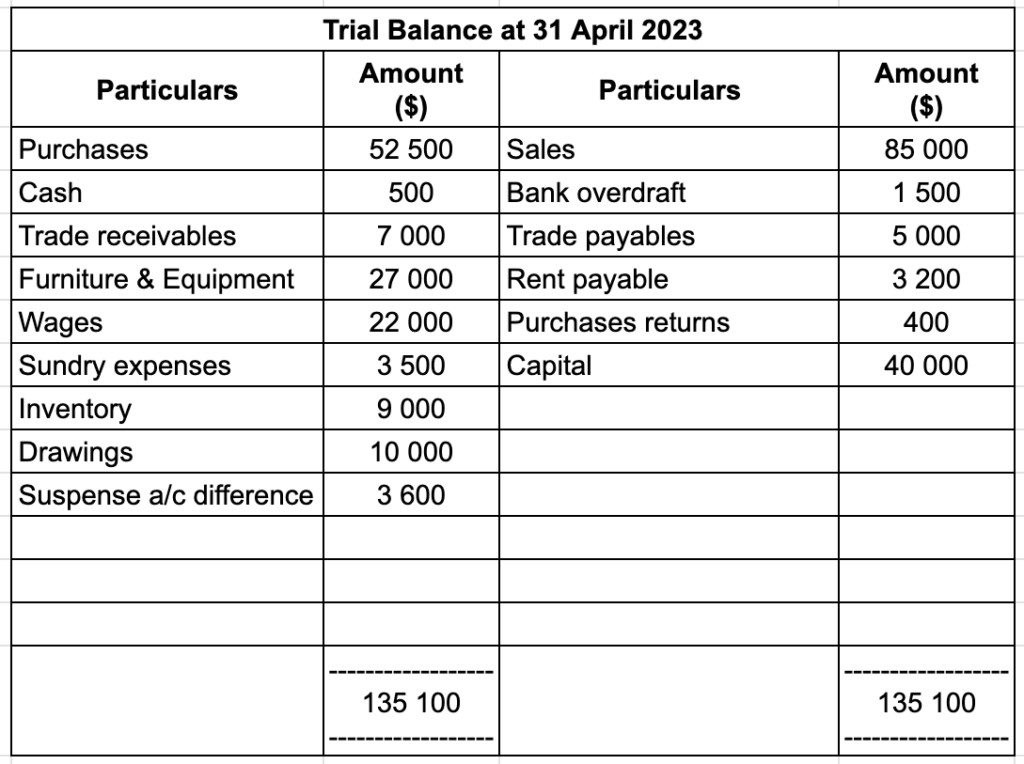

Vera is a trader. The following balances appeared in her books on 31 April 2023. Prepare Vera’s trial balance at 31 April 2023.

| $ | |

| Sales | 85 000 |

| Purchases | 52 500 |

| Bank overdraft | 1 500 |

| Cash | 500 |

| Trade payables | 5 000 |

| Trade receivables | 7 000 |

| Furniture and equipment | 27 000 |

| Wages | 22 000 |

| Sundry expenses | 3 500 |

| Rent payable | 3 200 |

| Purchases returns | 400 |

| Inventory | 9 000 |

| Drawings | 10 000 |

| Capital | 40 000 |

Answer

You know what to do. Identify the elements and their corresponding balances. (unless you’re a prodigy, I recommend writing it down one by one first).

| Particulars | Elements | Dr/Cr |

| Sales | Income | Cr |

| Purchases | Expenses | Dr |

| Bank overdraft | Liabilities | Cr |

| Cash | Asset | Dr |

| Trade payables | Liabilities | Cr |

| Trade receivables | Asset | Dr |

| Furniture & Equipment | Asset | Dr |

| Wages | Expenses | Dr |

| Sundry expenses | Expenses | Dr |

| Rent payable | Liability | Cr |

| Purchases returns | Income | Cr |

| Inventory | Assets | Dr |

| Drawings | Drawings | Dr |

| Capital | Capital | Cr |

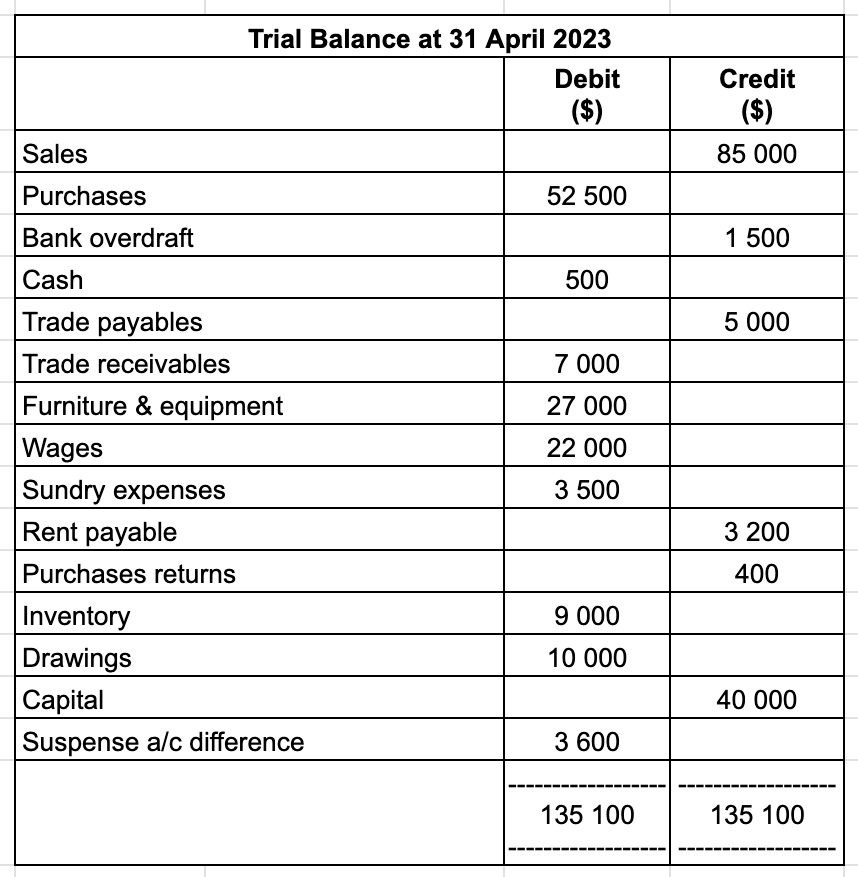

Now let’s put this in Trial Balance:

Another format, if we follow the textbook:

Trial Balance and Errors

When there are errors in your trial balance / if your trial balance fails to balance, it can be because of the following:

- an error of addition within the trial balance

- an error of addition within one of the ledger accounts

- entering a different figure on the credit to that entered on the debit when making a double entry in the ledger

- making a single entry for a transaction rather than double entry

- entering a transaction twice on the same side of the ledger

However, if a trial balance have the same amount of balance or its debit and credit side is equal, it can still mean that the double entries recorded are not completely free of error. There are 6 type of errors that may occur but cannot be revealed through a trial balance:

| Name of Error | Description of Error | Example |

| Error of commission | When a transaction is entered using the correct amount and on the correct side but in the wrong account | Cash received from Marji (as Income), but you credit the $ to Maddie’s a/c |

| Error of complete reversal | When the correct amount is entered in the correct accounts, but the entry has been made on the wrong side | Purchases debited to bank account and credited to purchases a/c (when you’re supposed to credit it from bank a/c and debit it in purchases a/c) |

| Error of omission | When a transaction has been completely omitted from the accounting records. | Payment for vehicle expenses not entered in books |

| Error of original entry | When a transaction is recorded with the wrong figures. | Drawings, $150, but recorded as $1500 |

| Error of principle | When a transaction is entered using the correct amount and on the correct side, but in the wrong class of account | Wages paid for installation of equipment is debited to wages a/c (it should be debited to equipment account instead) |

| Compensation errors | When two or more errors cancel each other out | Purchases account under-added by $200 and sales returns account over-added by $200 |

Check Out The Previous Topic!

https://prodatblog.org/igcse-accounting-topic-2-double-entry-book-keeping/

- Supply Side Policies – Get A* For Your Economics Exams! 101% (+ Extra Info On Dealing With Unemployment & Inflation)

- Chapter 3.5: Price Elasticity of Supply – Solid Sheet 100% Pass IB Exams

- Chapter 3.4: Income Elasticity of Demand – Fail Proof Summary 100% Pass IB Exams

- Chapter 3.3: Price Elasticity of Demand – Fast Recap 100% Pass IB Exams

- Unit 2.3: Leadership and Management – Guaranteed A* Student Success!