Table of Contents

Definition

Double entry system of book-keeping is the process of making a debit entry and a credit entry for each transaction. (Coucom, C. (n.d.). IGCSE & O-Level Accounting.)

Ledger Account

| Account Name | |||||

| Debit | Credit | ||||

| Date | Details | $ | Date | Details | $ |

For any Asset, Liability, Expense, Income, Debtor or Creditor, each of them have are recorded in separate ledger accounts.

Ledger account is a bound book where each account appears on a separate page. The left hand side is called debit (dr), while the right hand side is called credit (cr). (Coucom, C. (n.d.). IGCSE & O-Level Accounting.)

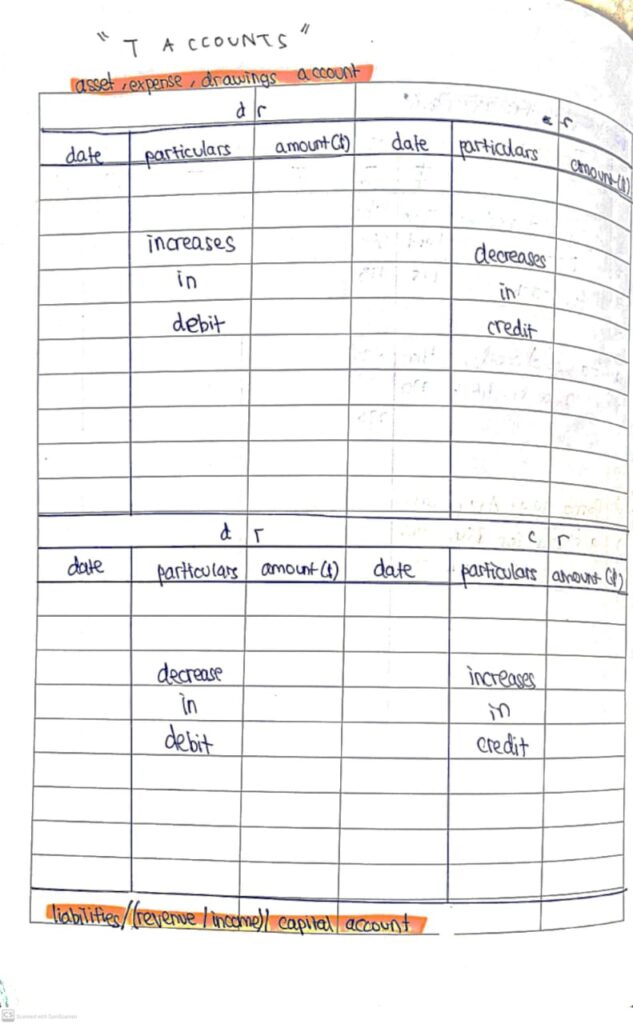

Rules of Accounts (Must Remember!)

Assets / Drawings / Expenses

- Debit side (Dr) for Increase

- Credit side (Cr) for Decrease

Liabilities / Income / Capital

- Debit side (Dr) for Decrease

- Credit side (Cr) for Increase

(if you don’t remember this, you will die. i guarantee.)

Double Entry Records for Assets and Liabilities

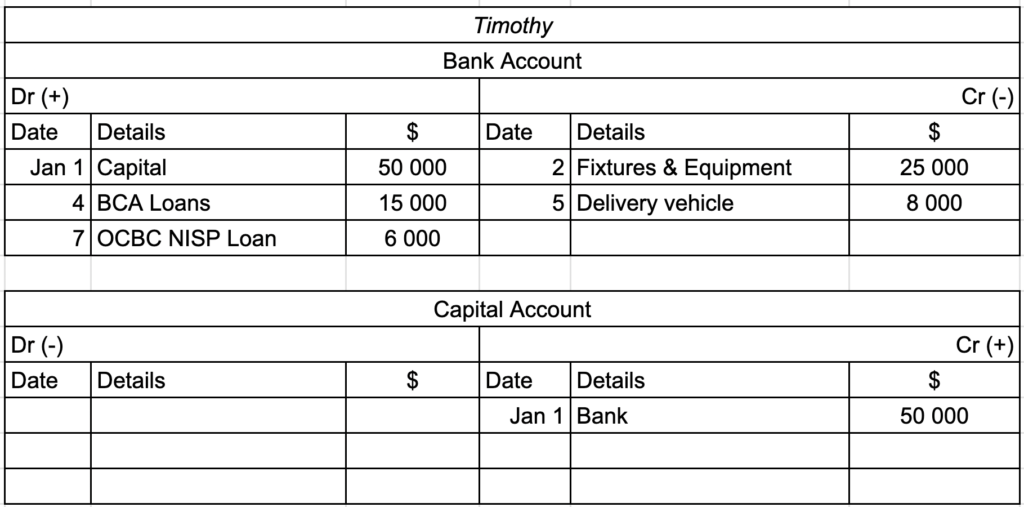

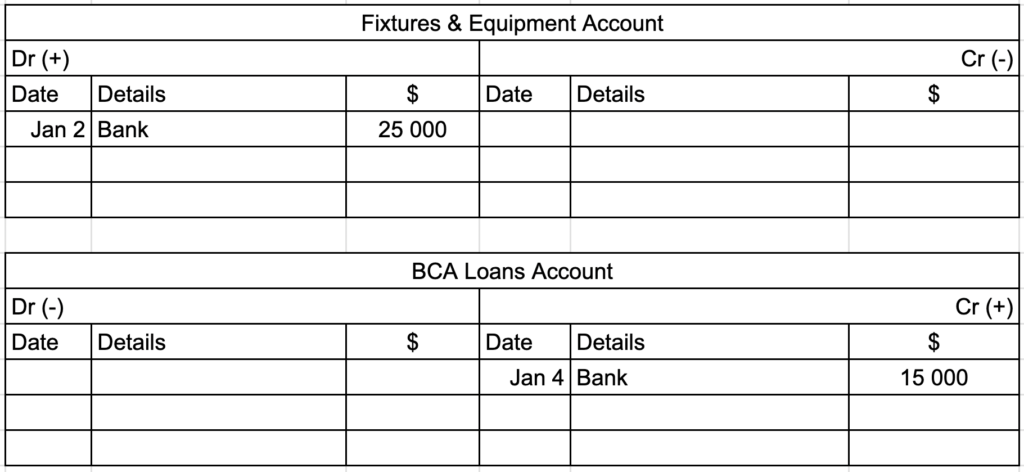

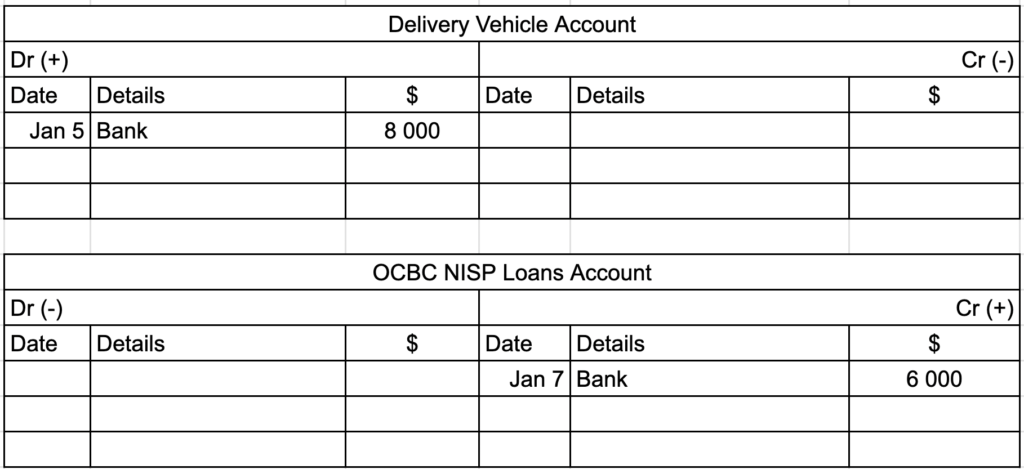

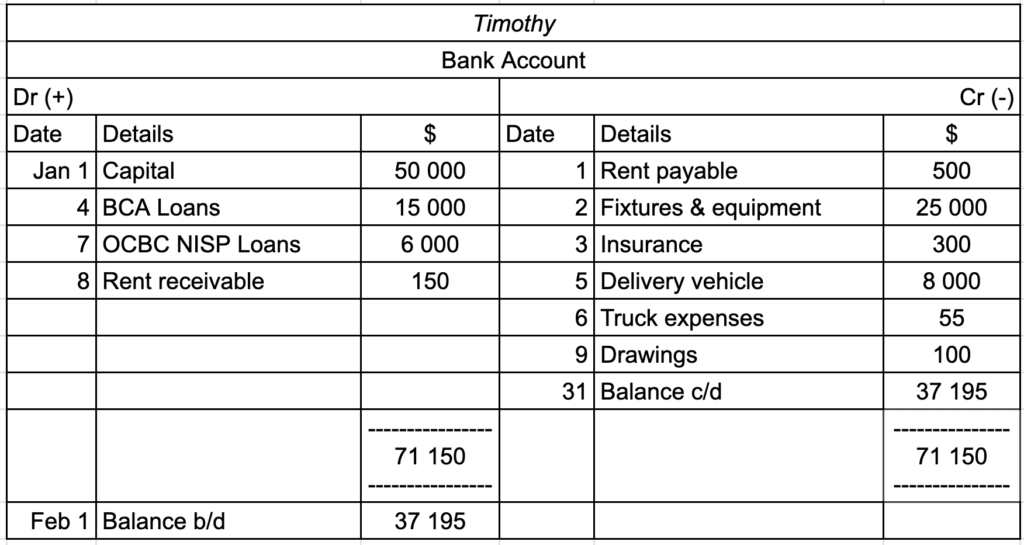

Example Question

| 2018 | |

| Jan 1 | Timothy opened his business. He invests $50 000 as capital into the business bank account. |

| Jan 2 | Fixtures and equipment cost $25 000 were bought and paid for by cheque. |

| Jan 4 | Short term loan of $15 000 was received from BCA Loans. |

| Jan 5 | Delivery vehicle costing $8 000 was bought and paid for by cheque. |

| Jan 7 | Long term loan of $6 000 was received from OCBC NISP. |

First, let’s identify the element of each of these transactions!

| 2018 | |

| Jan 1 | Capital -> investment |

| Jan 2 | Asset -> equipment |

| Jan 4 | Liability -> loan |

| Jan 5 | Asset -> vehicle |

| Jan 7 | Liability -> loan |

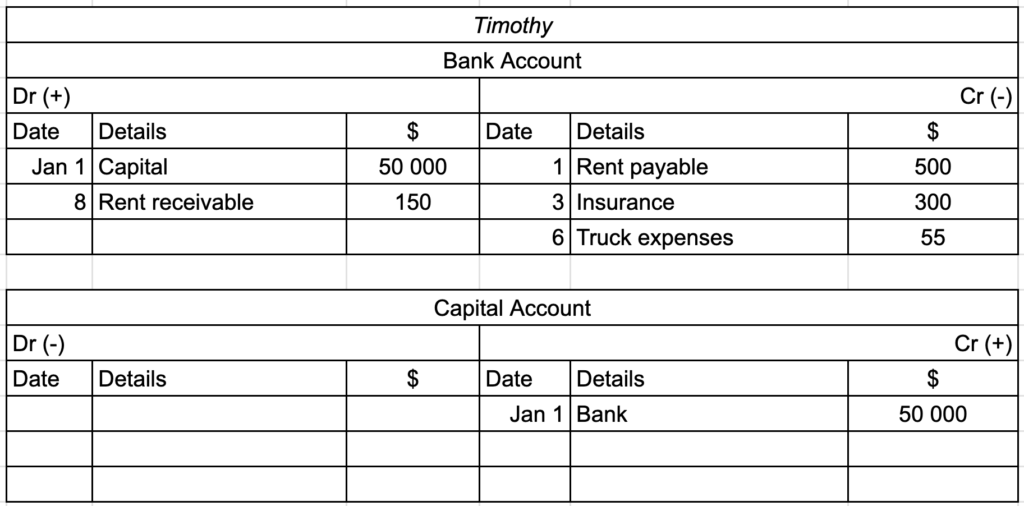

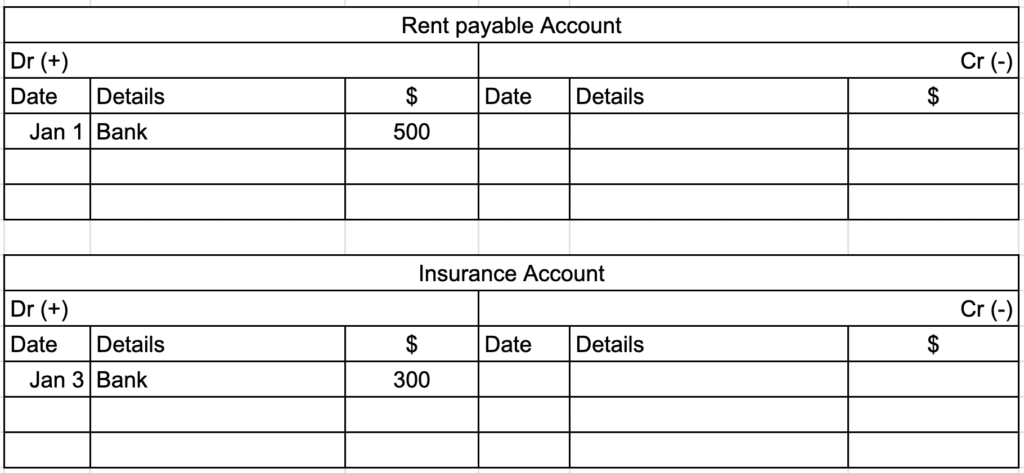

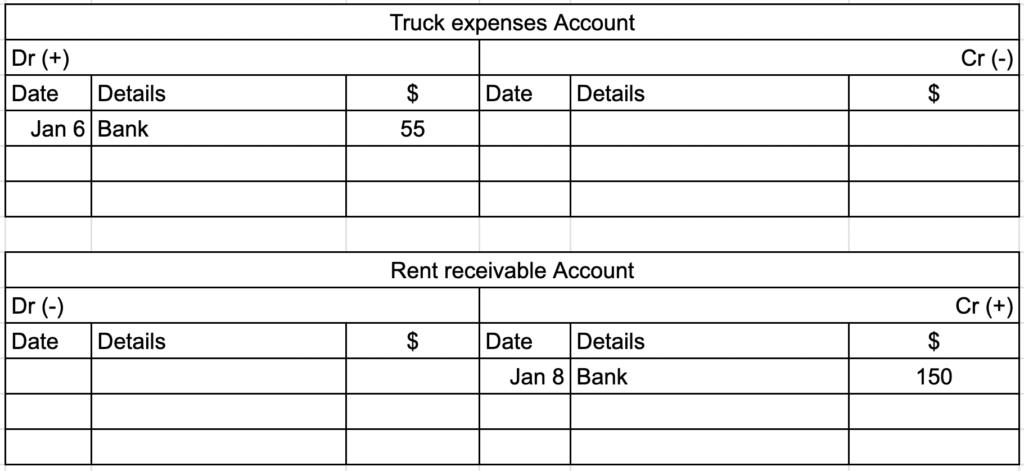

Now, let us enter the transactions above into Timothy’s ledger.

Double Entry Records for Expenses and Incomes

Example Question

| 2018 | |

| Jan 1 | Timothy opened his business. He invests $50 000 as capital into the business bank account. |

| Jan 1 | He paid rent of premises, $500, by cheque. |

| Jan 3 | He paid insurance, $300, by cheque. |

| Jan 6 | He paid truck expenses, $55, by cheque |

| Jan 8 | Part of the premises were rented out to another small business and received a cheque, $150. |

First, let us identify the element of each of these transactions!

| 2018 | |

| Jan 1 | Capital -> investment |

| Jan 1 | Expense -> rent payable |

| Jan 3 | Expense -> insurance |

| Jan 6 | Expense -> truck expenses |

| Jan 8 | Income -> rent receivable |

Now, enter the transactions above into Timothy’s ledger.

Double Entry Records for Drawings

Example Question

| 2018 | |

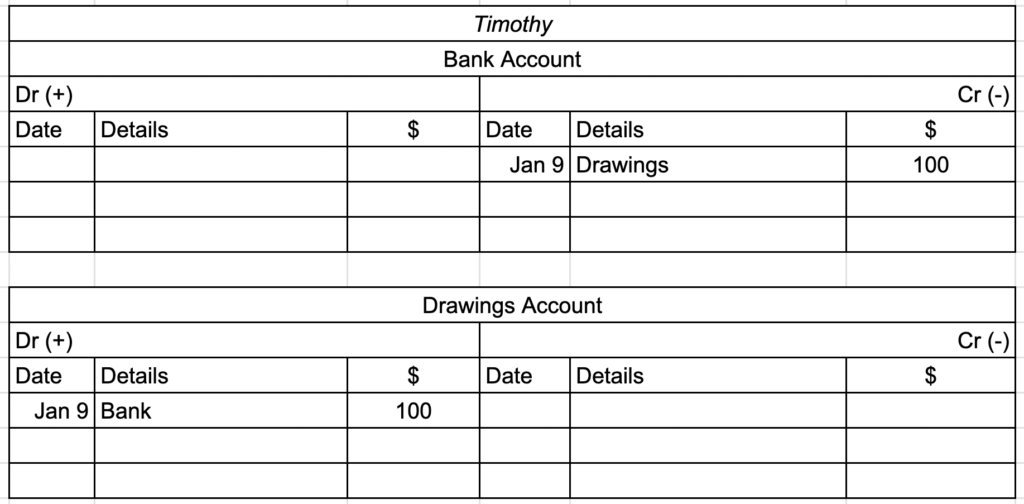

| Jan 9 | He took $100 cash from the business’ bank account for his own use. |

Identify the element!

| 2018 | |

| Jan 9 | Drawings -> own use |

Entering the transactions above into Timothy’s ledger.

Balancing Ledger Accounts

A Balance on a ledger account is the difference between the two sides of the account and represents the amount which is left in that account. (Coucom, C. (n.d.). IGCSE & O-Level Accounting.) It is usually abbreviated as balance c/d (balance carried down) and balance b/d (balance brought down) in accounting.

Ways to balance a ledger account:

- Total both debit and credit side of the ledger account.

- Enter the difference on the line below your written transactions, on the side which is lesser in amount.

- Beside it write the date (usually at the end of the month e.g. 31 Dec), and label it as balance c/d (carried down).

- Total both sides of the account and draw a line on top and below it, just to show that it’s the final amount. (compulsory!)

- Make the double entry for balance c/d. Write the amount on the opposite side of the next table, and label it as balance b/d. The date is usually at the start of the month, e.g. 1 Feb.

Example

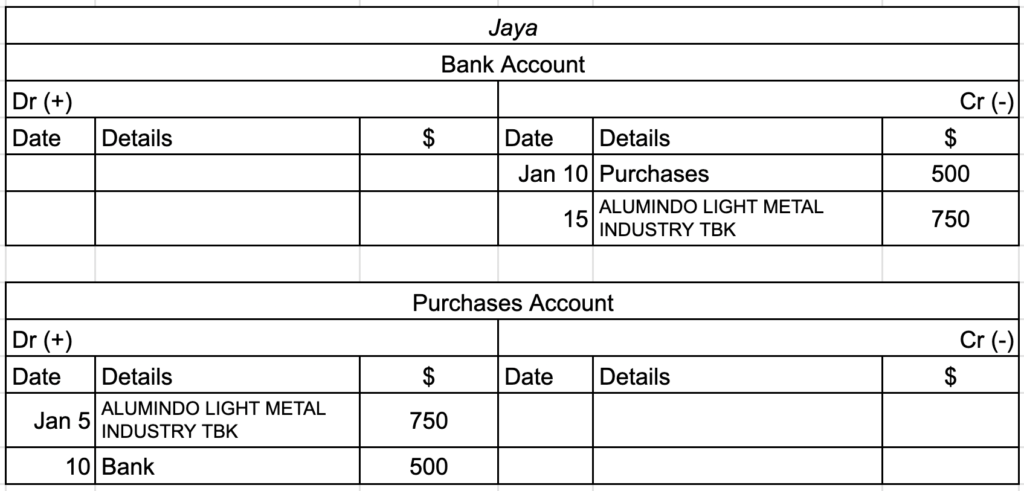

Double Entry Records for Sales, Purchases and Returns

Sales = goods sold by the business

Purchases = goods purchased for resale

Sales, purchases and its returns (i.e. sales returns or purchases returns) are recorded separately in accounting.

Purchases

- Bought on cash/cheque (immediate)

- Credit (buy first, pay later)

Example Question

| 2018 | |

| Jan 5 | Jaya bought goods on credit, $750, from ALUMINDO LIGHT METAL INDUSTRY TBK. |

| Jan 10 | Jaya bought goods on cheque, $500. |

| Jan 15 | Jaya paid the amount owing to ALUMINDO LIGHT METAL INDUSTRY TBK by cheque. |

Identifying the key points:

| 2018 | |

| Jan 5 | credit purchases (unpaid) |

| Jan 10 | purchases |

| Jan 15 | credit purchases (paid off) |

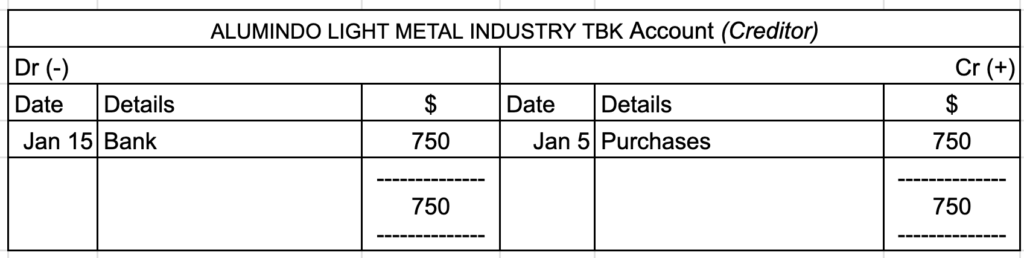

Now let’s put them in a ledger:

Why write date Jan 10 and not Jan 5 in Bank a/c?

Well, the purchase is not paid yet, so we can’t document the day the credit purchase was made in this account. Remember: Money has to go out first for it to be recorded as cash going out of bank.

POV: You are Jaya. ALMI is your creditor. Creditor account comes under Liability. So Debit (-) and Credit (+).

Why purchases credit?

Just take it as, when you buy goods on credit from someone, your debt on that business increases [In Indo: utang kamu sama Bisnis A tambah], so its credit (+).

Why bank debit?

If you pay off your debt/credit purchase towards that business, you insert that transaction as debit (-). [perumpaannya: utang kamu sama Bisnis A berkurang dan kamu bayar lewat cek].

Sales

- Sold on cash/cheque

- Credit (sell first, receive income later)

Example Question

| 2018 | |

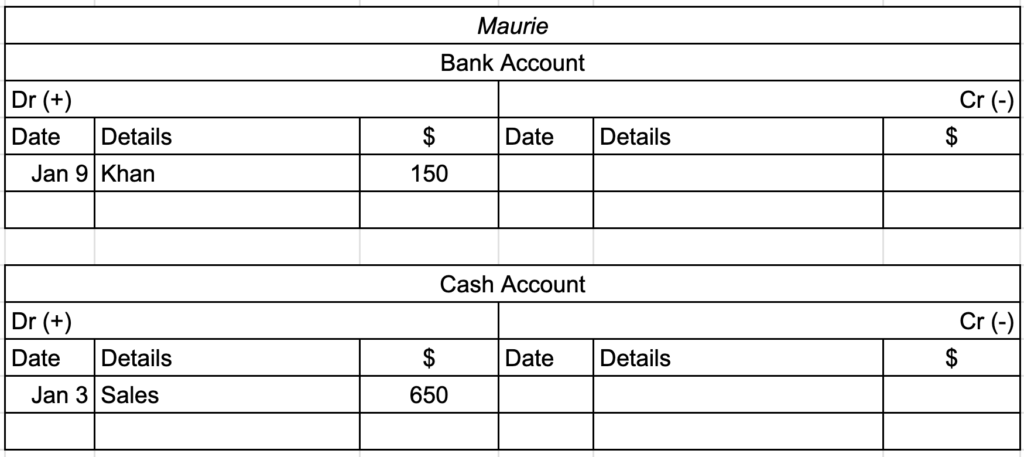

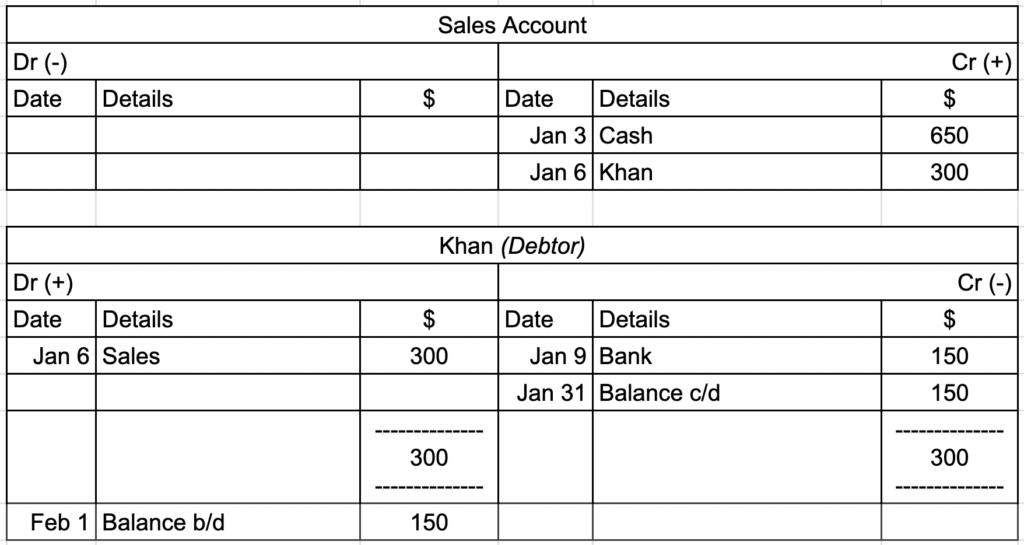

| Jan 3 | Maurie sold goods, $650, on cash. |

| Jan 6 | Maurie sold goods on credit, $300, to Khan. |

| Jan 9 | Khan gave Maurie a cheque for $150 on account. |

Identifying the main points of these transactions:

| 2018 | |

| Jan 3 | cash sales |

| Jan 6 | credit sales |

| Jan 9 | credit sales paid off by debtor |

Let us enter these transactions into Maurie’s ledger:

Sales Account is Income. So Dr (-) Cr (+).

Khan is your Debtor. He owes you money. So the initial amount of sales on credit made is added in debit side (his debt to you adds up on January 6th). But then he pays it off on January 9th, although just half. You credit the amount.

The leftover debt he needs to pay off is $150 in your books and so you put it as balance c/d at the end of this month and balance b/d the start of next month.

Returns

Purchases Returns

Faulty goods purchased by the business needs to be returned, we call this purchases returns or returns outward. In other words, this can count as expenses as goods/stock goes out of the business.

This amount will be credited in the purchases returns account of the business throwing away the goods, to show that money is going out.

However, in the books of the supplier of the good, the value will be debited to show goods coming in his/her business.

Sales Returns

When customers return your goods, you call that sales returns or returns inwards.

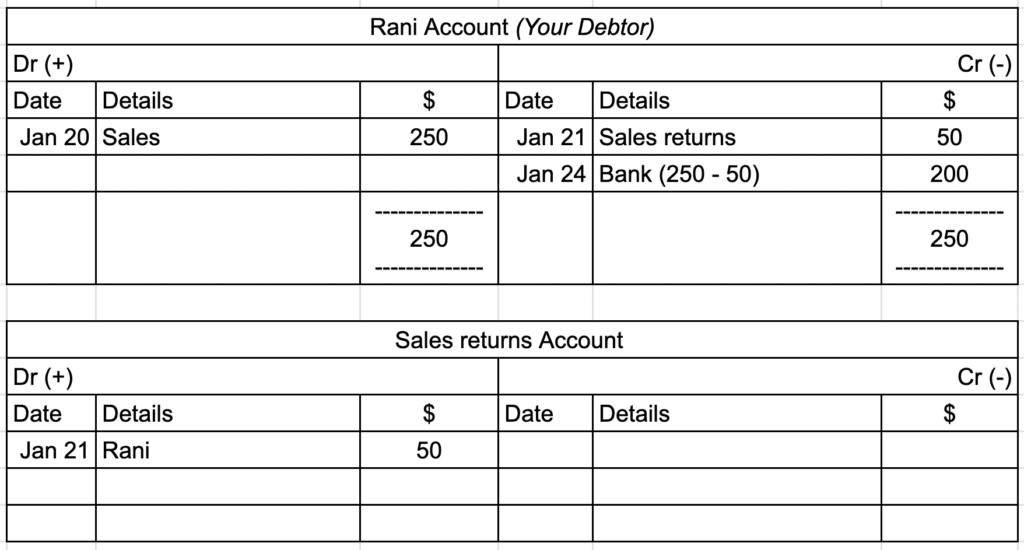

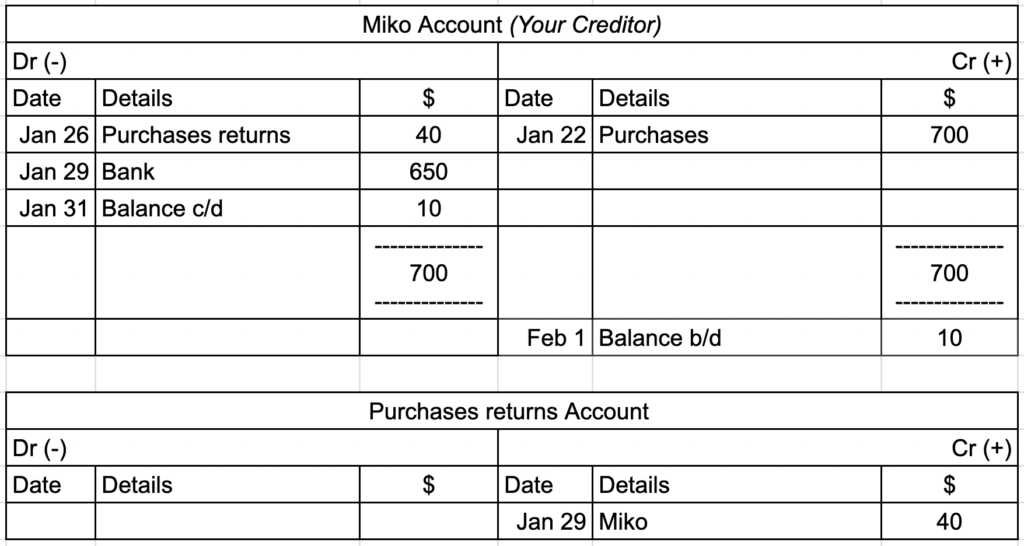

Example Question

| 2018 | |

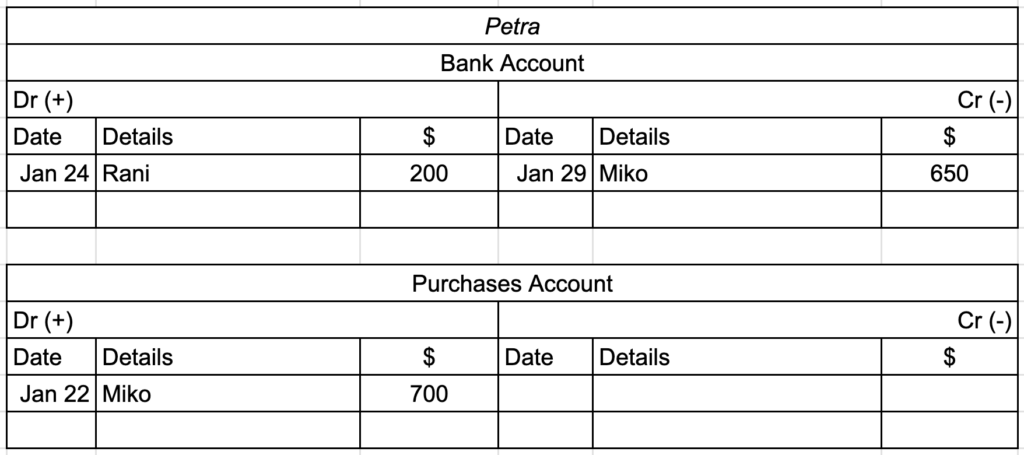

| Jan 20 | Petra sold goods, $250, on credit to Rani. |

| Jan 21 | Rani returned faulty goods, $50, to Petra. |

| Jan 22 | Petra purchased goods, $700, on credit from Miko. |

| Jan 24 | Rani paid their account by cheque. |

| Jan 26 | Petra returned damaged goods, $40, to Miko. |

| Jan 29 | Petra gave Miko a cheque for $650 on account. |

Okay, let’s identify the main points of these transactions first.

| 2018 | |

| Jan 20 | credit sales |

| Jan 21 | sales returns |

| Jan 22 | credit purchases |

| Jan 24 | credit sales paid off -> bank -> 250 – 50 = 200 |

| Jan 26 | purchases returns |

| Jan 29 | credit purchases paid off |

Let us enter these transactions into Petra’s ledger.

Sales returns Account will be opposite to Sales Account. So Dr (+) Cr (-). This is also counted as Expense.

Purchases returns Account is the opposite of Purchases Account. So, Dr (-) Cr (+). It has a credit balance to show that the business’ expenses are reduced. It is usually placed in the credit side of trial balance (you will learn this in Topic 3: Trial Balance).

Imagine that when you return faulty goods back to your supplier, he/she gives you back refund (so like a small sum of income); helps me remember that it is has credit balance.

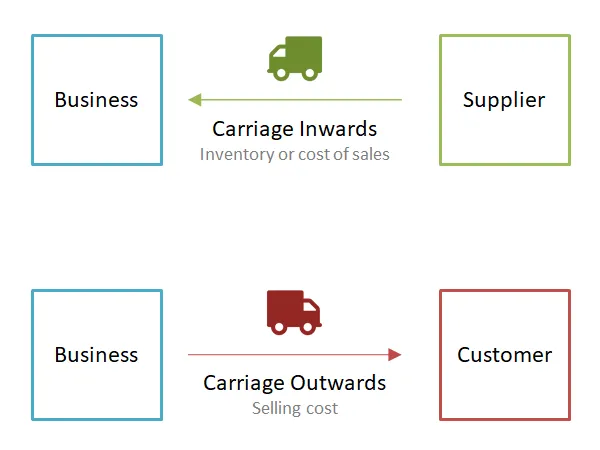

Double Entry Records for Carriage Inwards and Carriage Outwards

Carriage is the cost of transporting goods. In Bahasa Indonesia it’s called ongkir.

Carriage Inwards

You call this “cost of taking in goods into the business.”

How do we write the journal entry/How is the financial transaction recorded?

- Carriage Inwards Dr ($xxx) -> 💰 enters this a/c

Cash Account or Bank Account Cr ($xxx) -> 💰 leaves this a/c

Carriage Outwards

You call this “cost of delivering goods to customers.” (business can choose to pay for this)

How do we write the journal entry?

IF BUSINESS PAYS:

- Carriage Outwards Dr ($) -> 💰 enters this a/c

Cash Account or Bank Account Cr ($) -> 💰 leaves this a/c

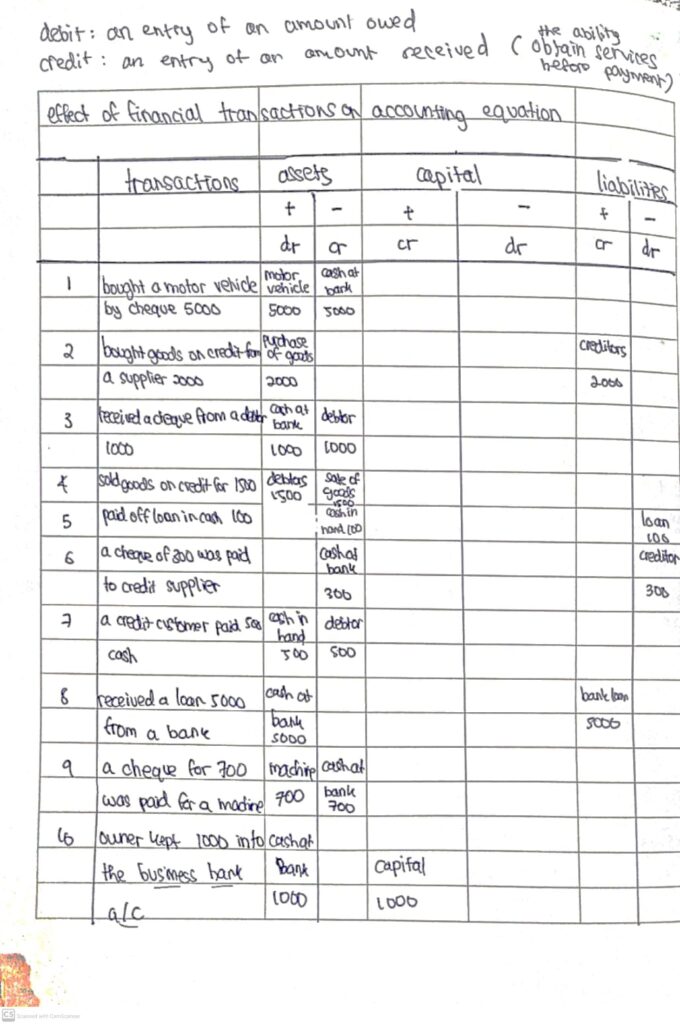

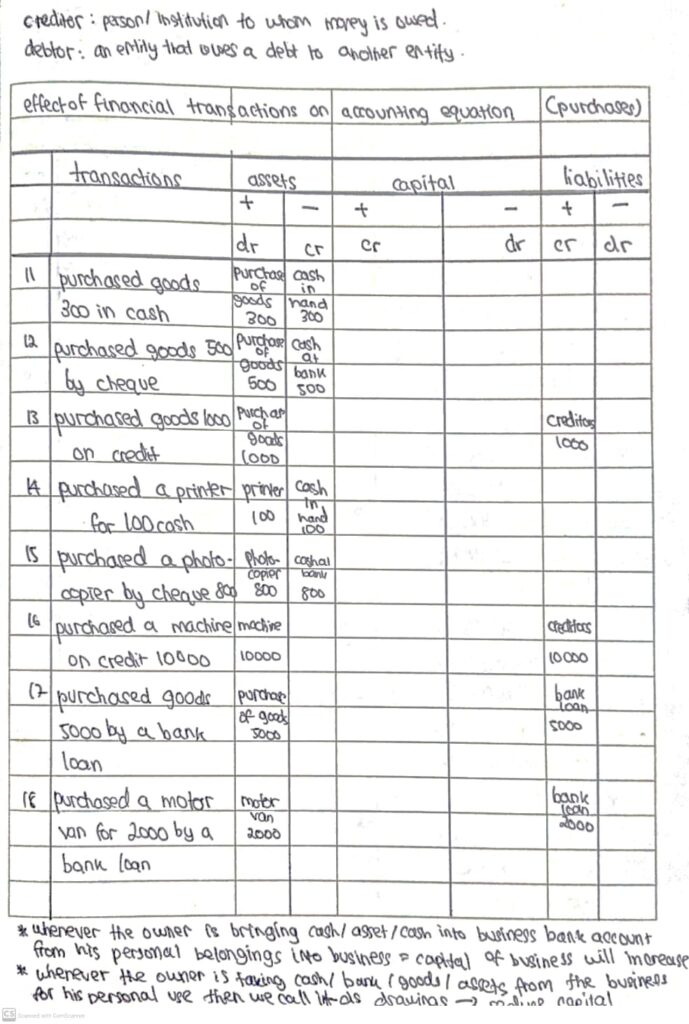

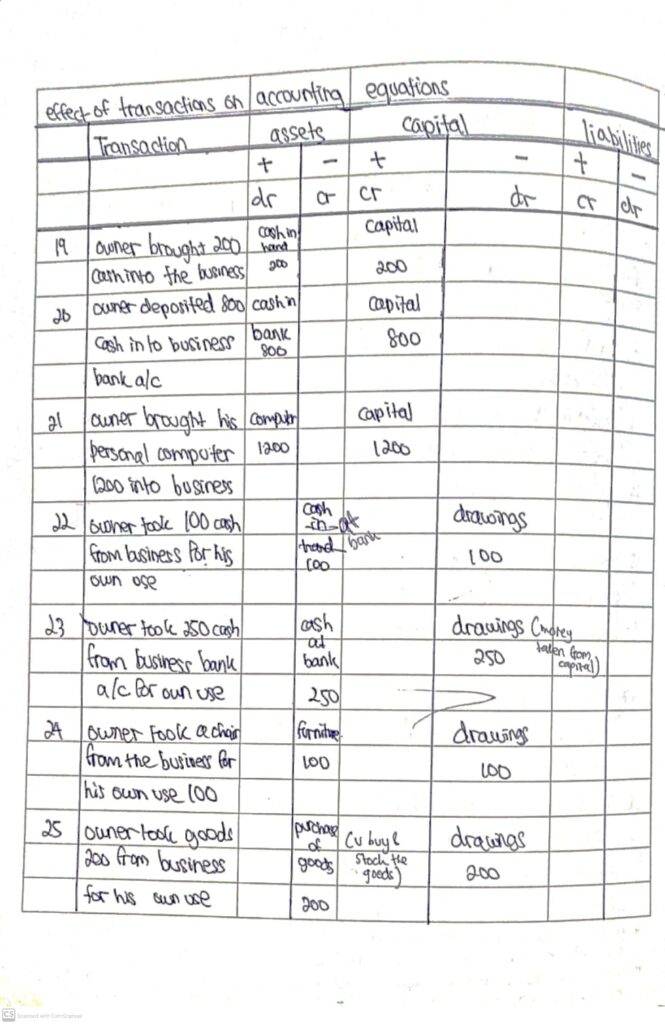

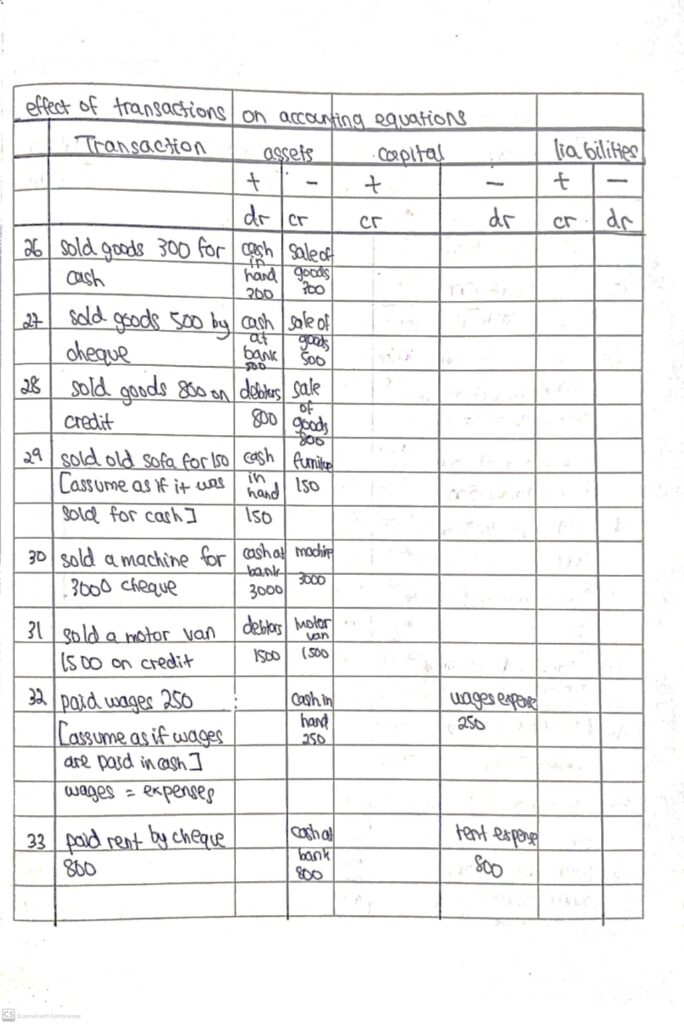

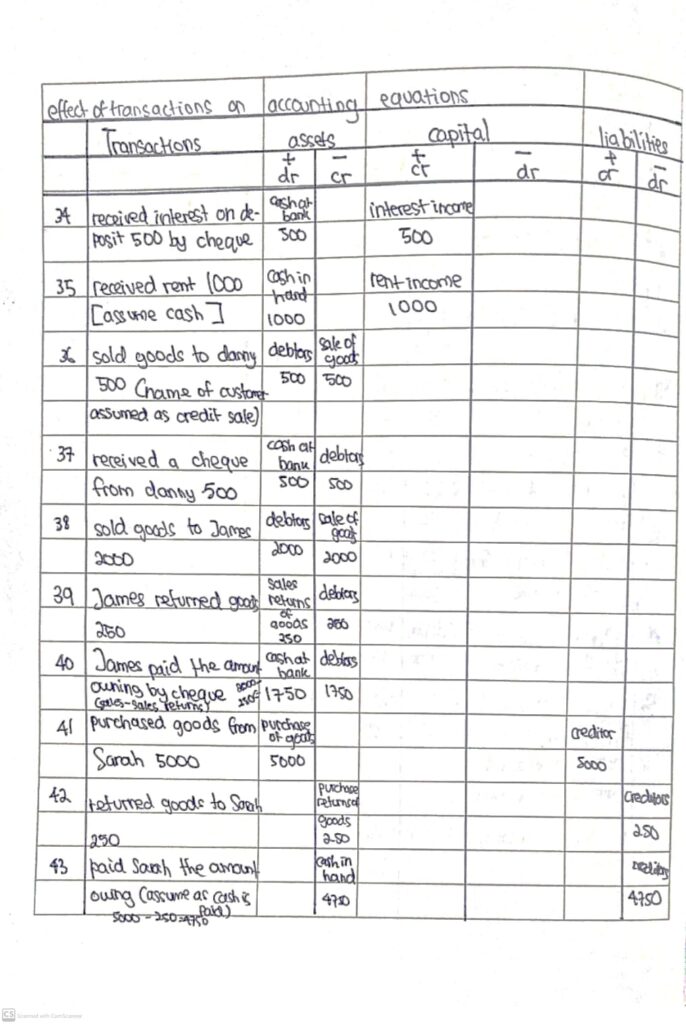

Notes – Journal Entries

Here are a few of my past notes about the effects of financial transactions on accounting equations. [FYI] Journal entries are the recording of financial transactions into books and ledger accounts. Example:

1) Bought motor vehicle and paid by cheque $500

So your journal entry will be:

Ans: Motor vehicles Dr 800

Bank Cr 800

As simple as that.

Now if you’re still confused like, “this one I put in which account ya.. “ or “this one what is the debit entry what is the credit entry..” Feel free to look into the attached notes I post below. Hope it helps!

You can test yourself too with by trying out the questions yourselves! ^^

Link to Topic 1: Basic Fundamentals Important For You To Know here!!

https://prodatblog.org/igcse-accounting-topic-1-essential-fundamentals/

- Supply Side Policies – Get A* For Your Economics Exams! 101% (+ Extra Info On Dealing With Unemployment & Inflation)

- Chapter 3.5: Price Elasticity of Supply – Solid Sheet 100% Pass IB Exams

- Chapter 3.4: Income Elasticity of Demand – Fail Proof Summary 100% Pass IB Exams

- Chapter 3.3: Price Elasticity of Demand – Fast Recap 100% Pass IB Exams

- Unit 2.3: Leadership and Management – Guaranteed A* Student Success!